About the Journal

History, focus, and scope

Escritos Contables y de Administración (ECA) is a biannual academic publication of the Departamento de Ciencias de la Administración, Universidad Nacional del Sur. It has been published from 1964 to 2005 under the name Escritos Contables, and its continuation seeks to contribute to the advancement and dissemination of scientific and technical knowledge of Accounting, Administration and other related disciplines.

The main purpose of ECA journal is the publication of original and unpublished scientific research articles, which disseminate the results of theoretical and/or applied studies on accounting, tax, administrative, financial issues and other areas of interest in the management of organizations.

Additionally, ECA journal has the following objectives:

- Communicate relevant advances in the fields of accounting, management, and related disciplines to the academic and professional spheres through book reviews, letters to the editor, guest author analyses, translations of documents with significant international impact, and other contributions;

- Promote the visibility of postgraduate research through summaries of doctoral and master's theses, as well as reviews of final specialization projects.

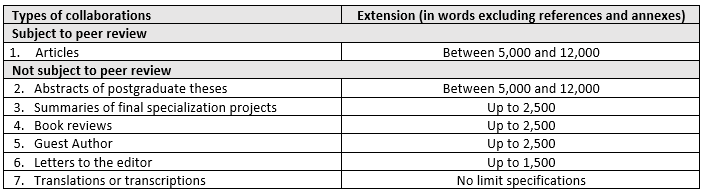

Types of collaborations

ECA journal receives various types of collaborations :

a) Collaborations subject to peer review

1. Articles

These may be empirical or non-empirical studies. An empirical paper is understood as a document that presents in detail the original results derived from basic and/or applied scientific research projects, using a quantitative, qualitative, or mixed approach. Empirical work includes case study designs: documents that present the results of research on one or more individuals, groups, organizations, communities, or societies, analyzed as a single entity. It explores a contemporary phenomenon (“case or cases”) in depth and within its real-life context. Among non-empirical studies, various types are accepted. A literature review is a document that analyzes, systematizes, or integrates published research results on a specific topic, with the aim of presenting the state of the art and identifying development trends. It is characterized by a thorough review of the literature. Theoretical/conceptual articles are documents that describe and/or examine existing concepts, variables, hypotheses, models, or theories, in relation to a new approach. Methodological articles are documents that introduce a new methodological approach or modifications to existing methods (they may use empirical data to illustrate the proposed approach). Articles analyzing and/or comparing regulations examine one or more specific standards or regulations, analyzing their motivation or purpose, historical background, main characteristics, and innovative or controversial aspects, among others. In comparative cases, regulations may be contrasted chronologically or across different jurisdictions (e.g., national vs. international). Reflective articles are documents in which the author analyzes a real-world phenomenon from a personal perspective, offering critiques and proposals grounded in a framework of previous work (theoretical, empirical, or by other authors). The description of article types is illustrative and not exhaustive.

b) Collaborations NOT subject to peer review

2. Summaries of postgraduate theses

Document that synthesizes part or all of the thesis work developed to qualify for a postgraduate degree -master's or doctorate- in the area of administration sciences, which have been defended and approved.

3. Summaries of final specialization projects

Document that synthesizes part or all of the work developed to opt for a specialization degree in the area of administration sciences, which has been defended and approved.

4. Book Reviews

Document containing critical presentations on the literature of interest in the publication domain of the journal.

5. Guest Author

Document that contains critical reflections on current and/or interesting issues in accounting, administration and related disciplines, made by recognized and experienced authors in the area invited by the Editorial Committee.

6. Letters to the editor

Document that contains critical, analytical or interpretative positions on the documents published in the journal, which in the opinion of the Editorial Committee constitute an important contribution to the discussion of the subject by the scientific community of reference.

7. Translations or transcriptions

Document that contains translations of classic or current texts, or transcriptions of historical documents or documents of particular interest in the publication domain of the journal.

c) Other collaborations

The Editorial Committee may accept other types of contributions it deems pertinent within the objectives, focus, and scope of the ECA journal. The Editorial Committee may decide to subject these contributions to peer review.

All submissions must adhere to the author guidelines and respect the length specified in the table below. The Editorial Committee reserves the right to accept longer contributions when deemed appropriate. Every contribution must include an abstract, keywords, and JEL classification codes in both the original language and their English translation.

Fees or charges

Accounting and Administration Writings does not charge authors any fees for sending and/or publishing articles.

Editorial process

The papers submitted for publication in the journal must be of high academic quality, result of a thoughtful and in-depth analysis that meets international evaluation criteria. This implies they have to approve the technical ruling process carried out by the Editorial Board and the academic ruling carried out by the specialists of the Scientific Committee or the ad hoc evaluators convened by the editor.

1) Reception and consideration by the Editorial Board

Once the submission is complete, the author receives an automatic email from the platform acknowledging receipt of the document (note: if you do not receive the notification in the inbox, check the spam folder). The reception of a manuscript does not imply its publication.

The manuscripts received are read by a member of the Editorial Board specialized in the subject of the article and, in case of doubt, the opinion of another member is requested. In the initial review, the Editorial Board evaluates the relevance of the topic, compliance with the presentation rules and ensures its originality using plagiarism detection software. If considered inappropriate for publication, the authors receive notification of the rejection decision. Otherwise, the double-blind evaluation process begins. Eventually, the Editorial Board may require adjustments in the collaborations before starting the arbitration.

2) Double blind peer review

Once the article passed the initial technical examination of the Editorial Committee, the process of academic ruling begins. All contributions are subject to the double-blind peer review process, except for approved postgraduate thesis summaries, approved specialization final project summaries, and book reviews. Double-blind review implies that the reviewers do not know the identity of the authors of the articles, and the authors do not know the identity of the reviewers.

For the types of manuscripts subject to review, after a positive evaluation by the Editorial Board, the double-blind arbitration process begins. For this, the document is sent to two external referees (that is, belonging to an institution different from the institutional affiliation of the authors), depending on their area of specialty. The evaluators have a period of 4 weeks to send their opinion. The result of the opinion can be:

- Publishable without modifications.

- Publishable with slight modifications.

- Publishable with substantial modifications.

- Not publishable.

When the opinions were not coincident, the resolution is as follows:

- Opinions 1-2, 1-3 or 2-3: it is requested to incorporate the proposed modifications.

- When one of the referees thinks that the work is not publishable (4), it is sent to a third referee. When there are three readers and two of them give a similar opinion (according to this criterion), the dissenting opinion is discarded.

Use of Generative Artificial Intelligence (GAI) in Peer Review. The peer review process is confidential, so information about it cannot be disclosed or transmitted to other individuals or institutions. Since GAI does not guarantee the safeguarding of information, the ECA journal requests that reviewers refrain from using these tools to analyze and comment on the papers assigned for evaluation.

The editor notifies the authors of the result of the evaluation process and, regardless of the types of opinions, sends the comments of the anonymous reviewers. It also sends the authors the report issued by the plagiarism detection software and requests the corresponding adjustments to safeguard the originality and proper citation of the sources. Likewise, the Editorial Board may request additional adaptations to issues considered pertinent and/or formatting aspects.

If it is publishable with modifications, the editor requests the authors to send the adjusted version of the manuscript, accompanied by a response letter to the reviewers and the Editorial Board in which they must exhaustively indicate which changes they incorporate and which ones they discard with their respective justification. Regarding the adjusted version of the article, the authors must make the modifications in red letters and mark the comments indicated in the document as resolved, avoiding deleting them.

Once the authors return the corrected version, the Editorial Board reviews the incorporation of the suggested modifications. It also sends the adjusted version to the referee(s) if they have requested it at the time of the evaluation. Ultimately, based on the entire evaluation process, the editor issues the final decision on the approval or rejection of the publication of the manuscript, and continues with the proofreading and layout stages.

The estimated average terms of the editorial processes described are as follows:

- Reception of the manuscript and initial evaluation of the Editorial Board: 30 days;

- Reception of the manuscript – Notification to the authors of the result of the double-blind arbitration: 120 days;

- Notification to the authors – Sending modified version: 20 to 40 days depending on the magnitude of the requested changes.

3) Style and layout correction

Manuscripts accepted for publication must go through a review and style correction process. The editor sends the authors an editorial diagnosis (Word file with track changes) showing the general observations and the changes that they should take into account. The authors review the changes proposed by the style editor and must return the Word file with the accepted/rejected changes, as they deem necessary. Abstracts in English are also subject to language review. This is the only phase of the process where the board admits minor changes to the content of the manuscript.

Once the layout process is complete, the editor sends the test version of the article in PDF format to the authors. The layout stage or galley test is intended to control formatting issues (tables, margins, typography, etc.) or minor errors that could have been unnoticed in previous instances (e.g. in affiliation data), but it does not admit suggestions that imply substantial modifications in the wording or content of the work. The authors review this proof and send the layout suggestions that they consider pertinent within the requested period.

4) Publication

The journal proceeds to publish the issue on its institutional page in PDF and HTML versions. It also disseminates the publication through the different databases in which it is registered.

Code of ethics and declaration of good practices

The Journal Accounting and Administration Writings is committed to meeting and maintaining the standards of ethical behavior at all stages of the publication process. With this aim, the members of the Editorial Board, authors and external evaluators adhere to the Code of Ethics and declaration of good practices, which is based on the Committee on Publication Ethics (COPE) Best Practice Guidelines for Journal Editors.

Open Access Policy

This journal provides immediate open access to its content, based on the principle that offering the public free access to research fosters further global knowledge exchange. Authors will retain their copyright and guarantee the journal the right to first publish their work, which will be simultaneously subject to the Attribution-Non-Commercial 4.0 International CC BY-NC 4.0 license.

Copyright Notice

Those authors who have publications with this journal accept the following terms:

- The authors will retain their copyright and guarantee the journal the right of first publication of their work, which will be simultaneously subject to the Attribution-Noncommercial 4.0 International CC BY-NC 4.0 license.

- The authors may adopt other non-exclusive license agreements for the distribution of the version of the published work (e.g.: deposit it in an institutional telematic archive or publish it in a monographic volume) provided that the initial publication in this journal is indicated.

- Authors are allowed and recommended to disseminate their work through the Internet (for example: on institutional or personal web pages) once their work has been published, which can produce interesting exchanges and increase the citations of the published work (See The effect of open access).

Digital preservation policies

The Journal Accounting and Administration Writings has an archival protection procedure integrated into the policy of the Central Library at Universidad Nacional del Sur. It has copies of OJS (code) and databases.

Privacy statement

The names and email addresses entered in this journal will be used exclusively for the purposes stated in it and will not be provided to third parties or used for other purposes.

Help sources

Departamento de Ciencias de la Administación, Universidad Nacional del Sur.

Indexation

Articles published in Journal Accounting and Administration Writings are indexed or summarized by:

- Núcleo básico

- DOAJ

- LATINDEX Catálogo v2.0 (desde 2018)

- LATINDEX Catálogo v1.0 (2002 - 2017)

- DIALNET

- Qualis CAPES

- REDIB

- LATINREV

- GOOGLE SCHOLAR

- ROAD

![]()

Plagiarism Policy

The articles sent to the Journal Accounting and Administration Writings are subjected to a plagiarism review process using the Duplichecker software. The detection of plagiarism will mean the automatic rejection of the articles.

Use of Generative Artificial Intelligence (GAI) in Academic Papers

When GAI tools are used in the development of research and/or manuscript preparation, authors must explicitly state this, detailing such usage in the methodology section (or a similar section) of the academic paper and in a section titled "Use of GAI," which should be placed at the end of the document, after the conclusions and before the references.

Specifically, authors must detail:

-

Which GAI tools were used, specifying their version (GAI tools evolve very quickly in terms of scope and accuracy) and for what purpose;

-

How they were used, including the details of prompts, context of use, and date.

Authors must also acknowledge and declare the potential limitations and/or biases of the GAI tools used in the manuscript.

If the information described above is too extensive, following good academic writing practices, it is suggested to include the essential details in the main body of the text and reference the full and detailed content in an appendix. Additionally, authors may use footnotes to indicate the use of GAI in the specific context, without replacing the full content that must be disclosed in the main text or appendix.

For more information on GAI policies in academic papers, we invite you to read the institutional resolution CDCA 191/2024 of the DCA, UNS, to which the ECA Journal adheres.